Should You Choose a £2000 Loan in the UK Instead of Credit Cards?

£2000 is that middle ground for borrowing? It is too much to brush off and pay back next month, but too small to feel like a major long-term debt. Both credit cards and personal loans are viable options. The right choice depends entirely on your personal circumstances, your habits, interest rates and your credit score.

Table of Contents

How Credit Cards Work for £2000 Spending?

Most people think they understand how credit cards work, but very few actually stop to break down what that means when you spend exactly £2000 on one. A credit card is a revolving credit line. Once you pay any part of the balance back, you can borrow that money again.

There is no fixed end date, and no fixed amount you have to pay back each month outside of the very small minimum. Your limit will almost always be higher than £2000, often much higher, even if you only applied to borrow that exact amount. Minimum payments are usually between 1% and 3% of your outstanding balance each month.

The interest is only ever charged on the remaining balance at the end of each statement period. The standard APR for most credit cards is between 18.9% and 39.9% for regular purchases, though you can get 0% purchase cards. This run between 12 and 28 months is completely interest-free.

- You will never get a letter telling you you are almost done paying

- You can choose to pay £100 one month and £20 the next

- The lender will almost never encourage you to pay the full balance off

- You can add extra spending to the same debt at any time

For almost every situation, you can run a direct side-by-side comparison of a £2000 direct lender loan in the UK vs a credit card and get a very clear picture of the total cost within two minutes. Most people just pick the option they are most familiar with, and never look at the numbers.

Interest Rate Comparison

This is the single biggest difference between the two options. The one that will cost you the most money if you get it wrong.

Personal Loans

A £2000 loan has a fixed interest rate that is agreed before you accept any money. This rate will never change for the full term of the loan.

For people with good credit rates start at around 6.9%, and go up to a maximum of 49.9% for people with very poor credit. For most applicants, the representative APR will fall between 9.9% and 19.9%.

The interest is calculated on the full original amount for the full term of the loan. You will know the exact total amount you will pay back, and the exact date you will be debt-free.

Credit Cards

The credit cards have standard variable rates between 18.9% and 39.9% for all applicants. 0% introductory offers are very common, and are one of the single cheapest ways to borrow money available if you use them correctly.

The interest is only ever charged on the balance you carry at the end of each month. If you pay the full balance off early, you will pay no extra interest at all. The single biggest catch is that once the promotional period ends, your rate will revert to the full standard rate, usually with no warning.

If you run the exact same repayment schedule against a £2000 direct lender loan in the UK vs a credit card, you will see which one works out cheaper, which changes based on how fast you pay the money back.

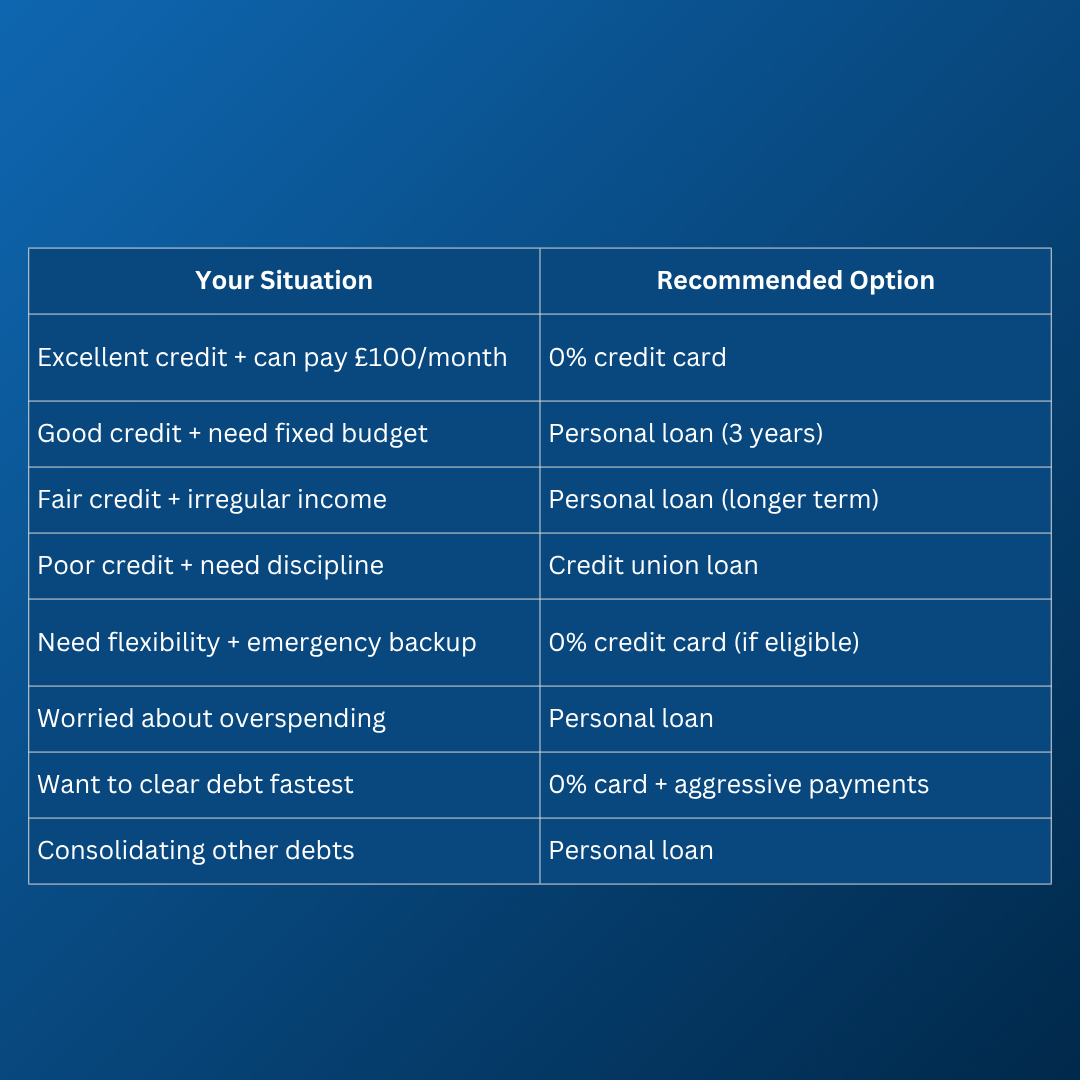

Decision Matrix – Which Should You Choose?

When A £2000 Loan Makes More Sense?

A loan is not better than a credit card for everyone, but it is better for many people. You should pick a loan if any of these apply to you.

A loan is the right choice if you want a structured repayment plan that you do not have to think about. It is the right choice if you know you have poor discipline with credit, and will be tempted to carry a balance longer than you need to.

It is the right choice if you want a completely predictable monthly budget, and want to know exactly how much will leave your account on exactly what day for the next year or two. It is the right choice if you do not qualify for any 0% credit card offers. It is the right choice if you want a fixed end date and want to be able to count down the months until you are completely debt-free.

It is the right choice if you do not want the ongoing temptation to reborrow the money again once you have paid it off. It is also the best option if you are consolidating multiple smaller existing debts into one single payment.

- You will never accidentally add an extra £50 takeaway to your debt

- No one can increase your limit

- You cannot extend the debt once it is set up

- You will get a clear final payment date on your very first statement

- There is no small print that can increase your cost halfway through

When Are Credit Cards Better?

A credit card is the right choice if you qualify for a 0% purchase card, and you are completely certain you can pay the full balance off before the promotional period ends. It is the right choice if you want maximum flexibility in how much you pay back each month.

It is the right choice if you think you might need access to a little extra credit beyond £2000 at some point in the near future. It makes a very good emergency fund backup that you can leave completely untouched unless you need it.

It is the right choice if you have very strong self-control with spending, and will actively overpay the balance whenever you can. It will also usually help you build your credit score faster with ongoing responsible use.

- You can pay the full balance off tomorrow and pay zero interest

- You can leave it unused, and it will cost you absolutely nothing

- You get automatic protection on almost everything you buy

- You can adjust your payments to match good and bad months

- You do not have to borrow the full £2000 all at once

Credit Score Impact

Both options will affect your credit score, but they affect it in very different ways and over very different timelines.

Personal Loans

A personal loan will leave a hard search on your credit file that will drop your score by a small amount for around 12 months. It will improve your credit mix. The fixed monthly payments are extremely easy to manage.

Once the loan is paid off, the account closes. The positive history will remain in your file for six years. It shows lenders you can manage instalment credit responsibly.

Credit Cards

A credit card will also leave an identical hard search on your file at the application. By far the biggest factor for credit cards is your utilisation ratio, and you should aim to keep this under 30% at all times to avoid damaging your score.

An open credit card will build a much longer positive account history. Missing a payment on a credit card is usually more damaging to your score than missing one on a loan.

Conclusion

The worst mistake you can make is picking the option that looks best on adverts, instead of the one that matches how you actually handle money. If you are certain you will clear the full balance within 24 months, get a credit card. If you would rather set a payment and never think about this debt again, get a loan.

John Milton is an experienced financial writer and personal loan expert with years of experience identifying the right category for people. He has been Chief Financial Expert at LoanChester in the UK and provides insights on the big deals of the lending institution. He is known for transforming the loan policies as per the unique needs of different borrowers. First, he focuses on what the borrowers require according to their favourable and adverse financial stances, and then he focuses on making a variety of personal loans affordable. John writes well-researched content on personal loans and also guides borrowers regarding their unique financial conditions. John holds a Ph.D. degree in banking and finance.